Profile:

Brown & Brown, Inc. is one of the largest independent insurance brokerage firms in the United States,

headquartered in Daytona Beach and Tampa, Florida. Founded in 1939, the company has grown to become the

sixth largest independent insurance brokerage, operating through three primary segments: Retail,

Programs, and Wholesale Brokerage. It offers a comprehensive range of insurance products and services,

including property and casualty insurance, employee benefits, and cyber insurance, serving a diverse

clientele that includes corporations, public entities, and individuals. Known for its commitment to

integrity, innovation, and customer service, Brown & Brown emphasizes principled customer focus and

disciplined risk management. Under the leadership of CEO J. Powell Brown, the firm has strategically

pursued growth through mergers and acquisitions while leveraging technology and data analytics to

enhance service delivery. With over 80 years of experience, Brown & Brown remains dedicated to

protecting what its customers value most and aims to be the leading global provider of insurance

solutions.

Market Overview:

The Insurance Brokerage Sector has been experiencing significant growth and transformation in 2024,

driven by increasing demand for risk management solutions and digital innovation. Here's an overview of

key players:

- Brown & Brown (BRO): Market Cap: $28.7 billion as of August 1, 2024. UP 22%

year-to-date, outperforming the broader market.

- Marsh & McLennan (MMC): Market Cap: $112.3 billion. MMC announced a major

acquisition of a cybersecurity insurance specialist, boosting its stock by 3.5% on the day of the

announcement.

- Aon PLC (AON): Market Cap: $75.6 billion. Key Event: Aon's innovative climate risk

assessment tool, launched in May 2024, has gained significant traction, contributing to a 7% stock

price increase over the past two months.

- Arthur J. Gallagher & Co. (AJG): Market Cap: $64.8 billion. Recent News: AJG

reported strong Q2 earnings on July 27, 2024, beating analyst expectations and driving the stock up

4.2% in the following trading session.

- Willis Towers Watson (WTW): Market Cap: $29.2 billion. WTW faced a significant

cybersecurity breach on June 30, 2024, which negatively impacted its stock price, causing a 5% drop.

The sector as a whole has been benefiting from increased demand for insurance products due to rising

natural disasters and cyber risks highlighted by the recent IT outage by prominent cybersecurity firm,

Crowdstrike. The S&P Insurance Select Industry Index has outperformed the broader S&P 500 by

5.8% year-to-date as of July 31, 2024.

Technological advancements, particularly in AI and data analytics, are reshaping the industry. Companies

investing heavily in these areas, like Brown & Brown and Marsh & McLennan, have seen stronger

growth compared to their peers.

Regulatory changes, including new cybersecurity requirements announced by the SEC in April 2024, have

also been driving demand for specialized insurance products and consulting services.

Acquisition Activities:

Just last week, July 29th, Brown & Brown announced its acquisition of Quintes Holding B.V. (serving

almost 200,000 customers in the Netherlands), highlighting Brown & Brown's commitment to expanding

its international footprint. This will not only help mitigate risks, but the diversification and

expansion into new markets will lead to increased revenue streams from different regions.

The consistent acquisitions by Brown & Brown signal strong growth potential, enabling the company to

expand its market share, diversify offerings, and achieve economies of scale. This approach is likely to

boost revenue and earnings, positively influencing the stock price as investors reward sustained,

profitable growth. The long-term impact on Brown & Brown's stock will depend on its ability to

integrate these acquisitions efficiently while maintaining a healthy balance sheet. This is not an issue

for the company as we can see the consistent acquisitions, growth, and proper integration.

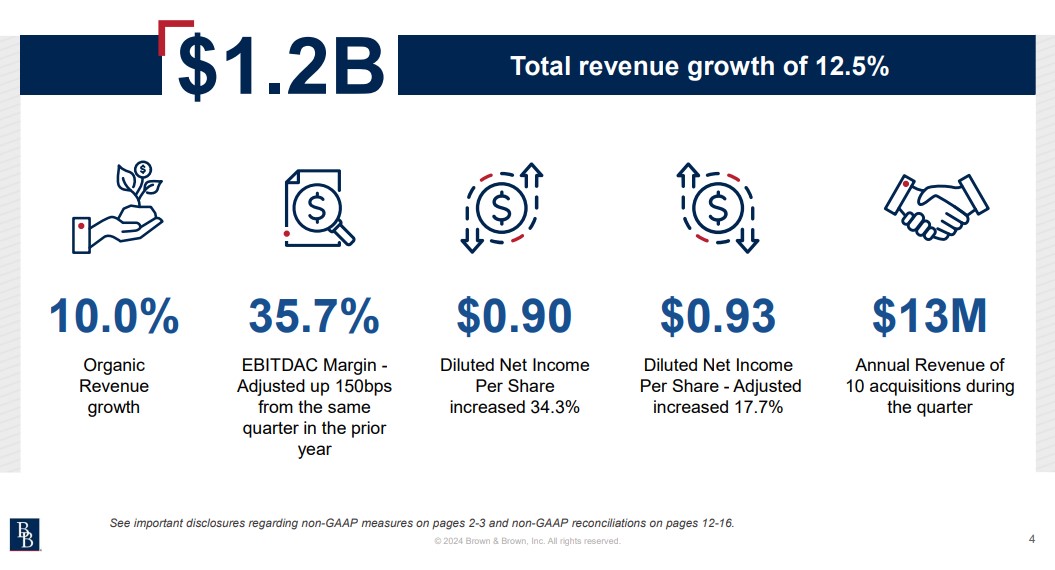

Overall - $13 Million Annual Revenue of 10 Acquisitions during this quarter

Some Prominent Acquisitions:

- June 7, 2024: Acquired the assets of McNamara Company.

- May 16, 2024: Two retail acquisitions - Garratts Insurance Brokers Limited and BNF

Insurance Services.

- March 13, 2024: Brown & Brown, Inc. acquired the assets of DealerMax.

- March 6, 2024: Acquired the assets of Hillco Insurance.

- February 6, 2024: Stewart & Partners was acquired by Brown & Brown (Europe)

Limited, becoming part of the Green Insurance Group.

- January 16, 2024: Bridge Specialty International agreed to acquire Singapore-based

Acorn International Network Pte Ltd.

Investment Strategy:

My investment strategy for BRO focuses on capitalizing on medium price appreciation.

- Profit Objective: Target a 15% - 25% price increase in the next 3 months based on

technical analysis.

- Stop-Loss: Implement a stop-loss order at 6% below the purchase price to limit

potential losses.

- Retest: Make sure to re-evaluate possibilities for further growth and appreciation

after the first target is met.

Note: Retesting is done with all ASP Portfolio Stocks, you can find updates in the

inbox on the

sidebar.

Rationale and Justification:

Financial Performance:

Brown & Brown has rallied 42.5% year-to-date, outperforming the insurance sector by 24.31% and the

S&P 500 by 27.7%.

Recent Q2 Financials beat EPS expectations by a whopping 0.05 (6.07% Surprise) and 12.5% Total Revenue

Growth.

Expecting Q3 & Q4 growth to stay consistent with Q1 & Q2.

Revenues for the six months ended June 30, 2024, under GAAP were $2.4 billion, increasing $272 million,

or 12.6%, as compared to the same period in 2023.

Brown and Brown Inc (BRO) Q2 Financials Summary

Risks:

Acquisition Integration Risks:

B&B’s focus on acquisitions poses risks when integrating new businesses and realizing expected

synergies. If integration challenges are not properly addressed, the company may struggle to achieve the

expected financial and strategic benefits. However, given B&B's consistent and robust acquisition

process, I believe they are well-equipped to overcome these challenges.

Dependence on Carrier Relationships:

Annual Reports: According to Brown & Brown's annual reports, a substantial portion of

the company’s revenue comes from commissions and fees related to insurance placements. For instance, in

their 2023 Annual Report, B&B noted that the majority of their revenue is derived from commissions paid

by insurance carriers, which are tied to the premium volume they manage to place with these insurers.

This highlights the importance of maintaining these relationships to ensure consistent revenue streams.

10-K Filings: In B&B's 10-K filings with the U.S. Securities and Exchange Commission

(SEC), the company explicitly acknowledges that its business relies heavily on its relationships with

insurance carriers. The filings typically state that if B&B is unable to maintain favorable terms with

these carriers or if these carriers decide to reduce their commission rates, it could have a material

adverse effect on the company's financial performance.

Industry Reports: A 2023 report by Deloitte on the insurance brokerage industry

highlights that brokers like Brown and Brown are particularly vulnerable to shifts in commission

structures, as they operate on relatively thin margins and rely on volume-based commissions to drive

profitability.

Carrier Decisions: There have been instances in the broader insurance brokerage industry

where carriers have reduced commissions or terminated relationships with brokers, leading to financial

strain. For example, in 2019, MetLife reduced commissions for some of its group insurance products,

which impacted brokers' revenue streams. Similarly, in 2021, Aetna made changes to its Medicare

Advantage plans' commission structure, leading to lower earnings for brokers handling these policies. If

similar actions were taken by a key carrier for B&B, it would likely experience a decline in revenue.

Conclusion:

Brown & Brown presents a compelling investment opportunity, driven by its aggressive acquisition

strategy, strong relationships with insurance carriers and consistent growth. The company's

consistent acquisitions signal a growth-oriented future, and as long as B&B continues to effectively

integrate these acquisitions while maintaining a healthy balance sheet, its stock price is poised

for long-term appreciation. Additionally, B&B's revenue model, heavily reliant on commissions from

insurance carriers, underscores the importance of maintaining these crucial relationships. The

ability to secure favorable commission rates is essential for the company's financial stability.

While any disruption in these relationships could pose risks, the company’s track record suggests it

is well-positioned to manage these challenges. My trading guidelines are meant as a guideline, pay

the price that coincides with your desired exit strategy and risk tolerance.